Jeb Bush said President Obama promised to lower health insurance premiums, but now “the president’s own team” says premiums will increase by “$2,900 over the next 10 years.” That’s misleading.

Obama did not promise to cut premiums; he promised to cut the rate of growth in premiums. As for future increases, the Centers for Medicare & Medicaid Services projects private insurance premiums per enrollee will rise by nearly $2,900 over nine years. But that is moderate growth by historical standards.

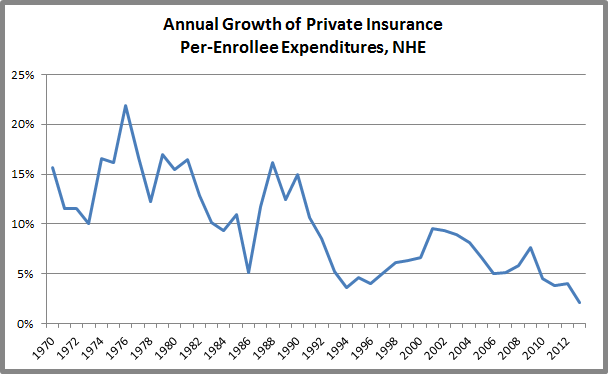

CMS’ National Health Expenditure Accounts, which has measured total health spending since 1960, expects premium growth to “remain modest” through 2018 and then grow faster due to stronger economic growth.

Bush, a Republican presidential candidate, made his remarks in New Hampshire on Oct. 13. The former Florida governor criticized President Obama for having promised that family premiums would go down by $2,500. Bush then gave an estimate for premium growth through 2024 that comes from the National Health Expenditure Accounts.

Bush, Oct. 13 (3:30 mark): Let’s look at what had been promised and what we got instead. President Obama promised health care insurance premiums that they would fall by $2,500 per family. Now it’s estimated by the president’s own team that they’ll increase by $2,900 over the next 10 years.

Bush’s comparison leaves the impression that a $2,900 increase over 10 years would be a marked departure from Obama’s promise. But it’s actually an apples-to-oranges comparison.

Years ago when Obama was making his $2,500-reduction claim, he didn’t always make it clear that he wasn’t talking about a straight price cut, but rather a slower growth of premiums than what would have happened without the ACA or other changes to the health care system. In other words, the president claimed that premiums would increase at a lower rate than they had been expected to before.

Bush’s $2,900 figure, meanwhile, is a straight increase, an estimate of premium growth per private health insurance enrollee.

We have no problem with Bush faulting the president for his broken promise — indeed, we’ve fact-checked Obama’s claim several times, calling his promise to lower premiums by about $2,500 “overly optimistic” and “misleading.” Obama even dropped it some time ago. His most recent misleading boast — this year — was that family premiums are “$1,800 lower today” on average than they would have been if premium trends that existed before the ACA had continued. As we’ve written before, it’s true employer-sponsored premiums have increased more slowly in recent years than they did before the ACA, but even the president’s own economic advisers say the law isn’t responsible for the entire slowdown.

In fact, in recent years, as the country has experienced low rates of overall health spending growth, experts with CMS have said that the ACA has had a “minimal” impact on that growth. Instead, CMS said it was largely the sluggish economy that impacted the growth of health spending. And while the latest report from those experts explains some impact from the ACA, it’s still the economy that will lead to an expected increase in that growth in the future.

Premium Growth

Bush gets his figure from the latest National Health Expenditures report, which was released in July and published in the journal Health Affairs. His figure is actually a nine-year increase, with private health insurance premiums per enrollee expected to go from $5,504 in 2015 to $8,389 in 2024 (see Exhibit 2). “Per enrollee” includes both primary policyholders and dependents. So, it’s not a measure of family premiums, but rather a per-enrollee average for all private health insurance, individual and family policies, taken together. And while most private insurance is employer-sponsored, these figures include spending for private plans sold on the individual market or through the state and federal marketplaces set up by the ACA.

The $2,900 increase over nine years would be an average 5.82 percent increase in per-enrollee premiums per year.

How does that compare to the years before? The NHE report says the per-enrollee private health insurance expenditures were $3,938 in 2007. That means they grew an average of 5 percent per year from 2007 to 2015.

Most of that time period is still under Obama. If we look at pre-Obama numbers from the NHE’s historical charts, the average annual growth is higher: It was 9.4 percent per year from 2000 to 2008 (see Table 21).

CMS’ experts did cite some impact from the ACA on private health insurance spending in their most recent report. The report said: “The implementation of the health insurance Marketplaces, which provide many Americans with access to new or more generous coverage, contributed substantially to faster projected growth in private health insurance premiums and benefits in 2014.” But that growth was “somewhat moderated” by an increasing use of high-deductible health plans by employers.

CMS said that private insurance enrollment is expected to grow by 5.4 million between 2015 and 2018, but that “the growth rate of per enrollee private health insurance premiums is expected to remain modest, at 4.1 percent.” CMS again cited an increasing use of high-deductible insurance plans as one factor, as well as insurers offering more narrow-network plans, and, starting in 2018, some employers switching to lower-cost plans to avoid an ACA excise tax on high-cost health plans.

After 2018, the rate of growth is expected to pick up, in a delayed response to economic growth.

“National Health Expenditure Projections, 2014-24,” Health Affairs, July 2015: Expected stronger economic growth in 2017–19 is anticipated to result in a lagged increase in the growth of health expenditures, since increases in the use of health care goods and services typically follow periods of faster growth in disposable personal income. Accordingly, private health insurance premiums are projected to increase faster in 2019–24 than in 2016–18: 5.6 percent versus 5.1 percent (Exhibit 2).

Bush is right to fault Obama for not living up to a campaign promise that he has since stopped promising. But Obama’s $2,500-decrease isn’t in direct contrast to expected future growth in premiums, which were always expected to continue to rise and, in fact, have risen at a moderate rate.